In recent times, Canadian households have seen a notable increase in their debt-to-income ratios. As of the first quarter of 2023, this ratio reached an alarming 184.5%, indicating that Canadians owe nearly $1.85 for every dollar of disposable income. A study by RBC highlighted that individuals between the ages of 35 and 44 have an even more daunting ratio, with debts totaling 250% of their disposable income. Millennials are not far behind, with their debts constituting 165% of their income.

This surge in debt levels primarily stems from significant increases in mortgage balances driven by unprecedented demand in the housing market. This article delves into the nuances of Canadian debt across various demographics, providing insights into how debt accumulates differently depending on one’s age.

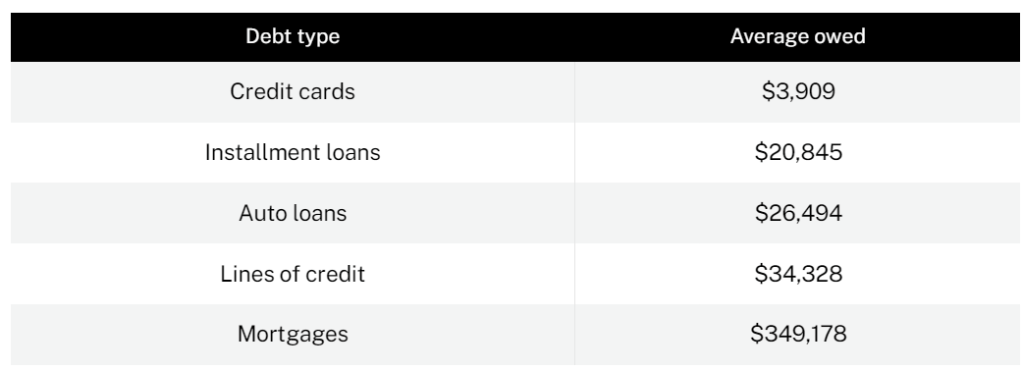

TransUnion’s Q1 2023 Credit Industry Insights

Understanding Debt Across Different Age Groups

- Young Adults (18-29 Years Old): Young Canadians, particularly Gen Z and young Millennials, are entering the housing market, often taking on substantial mortgages. The average mortgage balance for this group stands at around $475,318. Additionally, they tend to carry credit card debts with an average balance of approximately $4,500, and those with home equity lines of credit (HELOC) owe about $55,000 on average.

- Thirties (30-39 Years Old): Individuals in their thirties are likely to have purchased homes recently, resulting in significant mortgage debts. The total debt for this age group averages around $644,000, spanning mortgages, HELOCs, credit cards, and student loans. The average mortgage debt alone for this cohort is over $500,000.

- Forties (40-49 Years Old): This demographic is often at the peak of their indebtedness, balancing large mortgage balances and lines of credit. The total average debt for people in their forties is nearly $648,000, with HELOCs averaging over $102,000 for those who have them.

- Fifties (50-59 Years Old): As individuals approach retirement, there’s a concerted effort to reduce debt levels. The average mortgage debt for those in their fifties is about $367,000, contributing to a total debt load of approximately $566,000.

- Sixties (60-69 Years Old): Heading into retirement, it’s advisable to be mortgage-free; however, many still carry significant mortgage balances averaging $256,000, with total debts around $436,000.

- Seventies and Beyond (70+ Years Old): Even in their 70s, many Canadians still bear mortgage and HELOC debts. The average mortgage debt remains substantial at $217,500, and those with HELOCs owe more than $124,000 on average.

The Broader Economic Context

These figures emerge against a backdrop of rising interest rates intended to curb inflation. This monetary tightening has increased mortgage and debt repayments significantly, stretching many Canadians’ financial capabilities. Additionally, factors like low savings rates, rising taxes, and nominal wage increases that do not match the pace of inflation further complicate the financial landscape for many.

Navigating Financial Pressures

For Canadians grappling with high debt levels, understanding where their money is going is crucial. Budgeting and tracking expenses can provide clear insights into necessary adjustments, potentially easing the burden of debt. Tools and resources are available to help manage and possibly reduce debt, ensuring a more secure financial future.

In conclusion, while the debt situation in Canada presents challenges across generations, understanding and proactive management can help mitigate its impact, ensuring Canadians can transition from surviving to thriving despite economic pressures.

source: How much debt is normal in Canada? We break it down by age – MoneySense

Leave a comment